Frances Grant had a burgeoning restaurant business,

Fran’s Kitchen, located at 2000 Brooklyn Ave. in Fort Wayne. Her specialty is soul food—greens, yams, dressing, and the like. Along the way, she’s earned a reputation for friendly customer service with a smile.

Then the pandemic hit, and Grant had to exhaust her financial reserves to cover the loss of business. She talked to her friend, Nakia Jackson, who also owns a restaurant, Zeb’s Chicken Shack. Jackson and her business partner had received a loan from the

local social services agency, Brightpoint, through their small business lending program.

As a result of this connection, Grant got in touch with Brightpoint, too, and was able to secure a loan for Fran's Kitchen. The funding allowed her to regain her bearings from the pandemic and think about the next steps in her business’s trajectory.

![]() Frances Grant has a burgeoning soul food business, thanks in part to Brightpoint’s investment in her enterprise.

Frances Grant has a burgeoning soul food business, thanks in part to Brightpoint’s investment in her enterprise.Grant is among dozens of small business owners who have benefited from Brightpoint's designation as a Community Development Finance Institution (CDFI). CFDIs, which can be banks, credit unions, loan funds, microloan funds, or venture capital providers, offer an alternative to traditional lending and play an essential role in generating economic growth and opportunity in some of the nation's most underserved communities.

Brightpoint is the first CDFI in Northeast Indiana, starting in 2010, and it has already made dreams within reach for many low-resource individuals, particularly during the pandemic and subsequent national inflation.

So how do CDFIs work? They offer tailored resources and innovative programs that invest federal dollars in businesses alongside private sector capital. In this way,

CDFI funds create "opportunities for borrowers and communities that have been historically denied access to mainstream sources of credit and that have increasingly been targeted by high-priced or predatory loans." They serve as mission-driven financial institutions, which take a market-based approach to supporting economically or socially disadvantaged communities.

Brightpoint’s president and CEO Steve Hoffman says the organization is doing just that by using funds to help low-income entrepreneurs and people in specific census tracts in Northeast Indiana get a business off the ground or expand.

“Those program (requirements) are very clear,” Hoffman says. “There are different ways to potentially get a loan from us. But when people have come to us, they have usually exhausted all other lending options.”

![]() Brightpoint President/CEO Steve Hoffman, right, was on the podcast of Mayor Tom Henry, left, earlier this year to discuss the agency’s impactful work.

Brightpoint President/CEO Steve Hoffman, right, was on the podcast of Mayor Tom Henry, left, earlier this year to discuss the agency’s impactful work.In this way, Brightpoint takes a chance on people who are often seen as "on the margins" by traditional banks, investors, or lenders. According to statistics supplied by the agency, about half of their clients are People of Color. About two-thirds are women. Most are under age 50.

However, the similarities end there. There’s variety in terms of the nature of the enterprises funded.

“We can fund almost any kind of business,” Hoffman says. “We've got a lot of single-proprietor type businesses, but also storefronts, restaurants, hairdressers—all sorts of different kinds. But a lot of them are startups or very young. In this case, they're trying to take the next step toward sustainability.”

According to Hoffman, Brightpoint can help a business owner take the next step by providing a loan up to $50,000. That money can be spent on equipment, rent, working capital, marketing, and other specified expenses. Usually, the terms of the loans are from one to six years and interest falls between 5 and 7 percent.

A support network

Hoffman acknowledges that the interest rate on Brightpoint's CDFI might be higher than a traditional bank loan, due to no credit, poor credit, or other circumstances. However, Brightpoint is often willing to work with recipients on repayment and restructuring the loan terms. The agency also acts as a support system outside of the scope of the lending aspect.

“We’re looking at ways we can continue to support the borrower's business, beyond just giving them access to finding financial capital,” says Matthew Crouch, Vice President of Community Economic Development for Brightpoint. “For example, that means we might look at other kinds of training to help them. Maybe they need to hire a consultant to help them. Or maybe they need to get connected to marketing assistance.”

Whatever the need, Crouch says they can either help business owners internally or direct them to other resources in the local entrepreneurial ecosystem, such as

SEED Fort Wayne, the NIIC, Start Fort Wayne, or Purdue University Fort Wayne.

Ultimately, when small businesses succeed in Fort Wayne, everyone wins.

“These small businesses are typically owned by low-income individuals who are trying to get out of poverty and make a better life for themselves,” Crouch says.

Expanding opportunities

Brad Little is President and CEO of the Community Foundation of Greater Fort Wayne, and he’s familiar with this plight. He shares insights gleaned from visits to other cities over the years. For instance, Louisville, KY, has several CDFIs doing work in the community and effecting change on the small business level.

![]() Brad Little, right, and Alison Gerardot, left, of the Community Foundation of Greater Fort Wayne spent 36 hours touring Louisville by bus.

Brad Little, right, and Alison Gerardot, left, of the Community Foundation of Greater Fort Wayne spent 36 hours touring Louisville by bus.“We've learned that the CDFI strategy has been a really important ingredient to not just the overall success of the entrepreneurial community, but in particular, the minority, Black entrepreneur, or BIPOC entrepreneur who is struggling for access to traditional funds,” Little says.

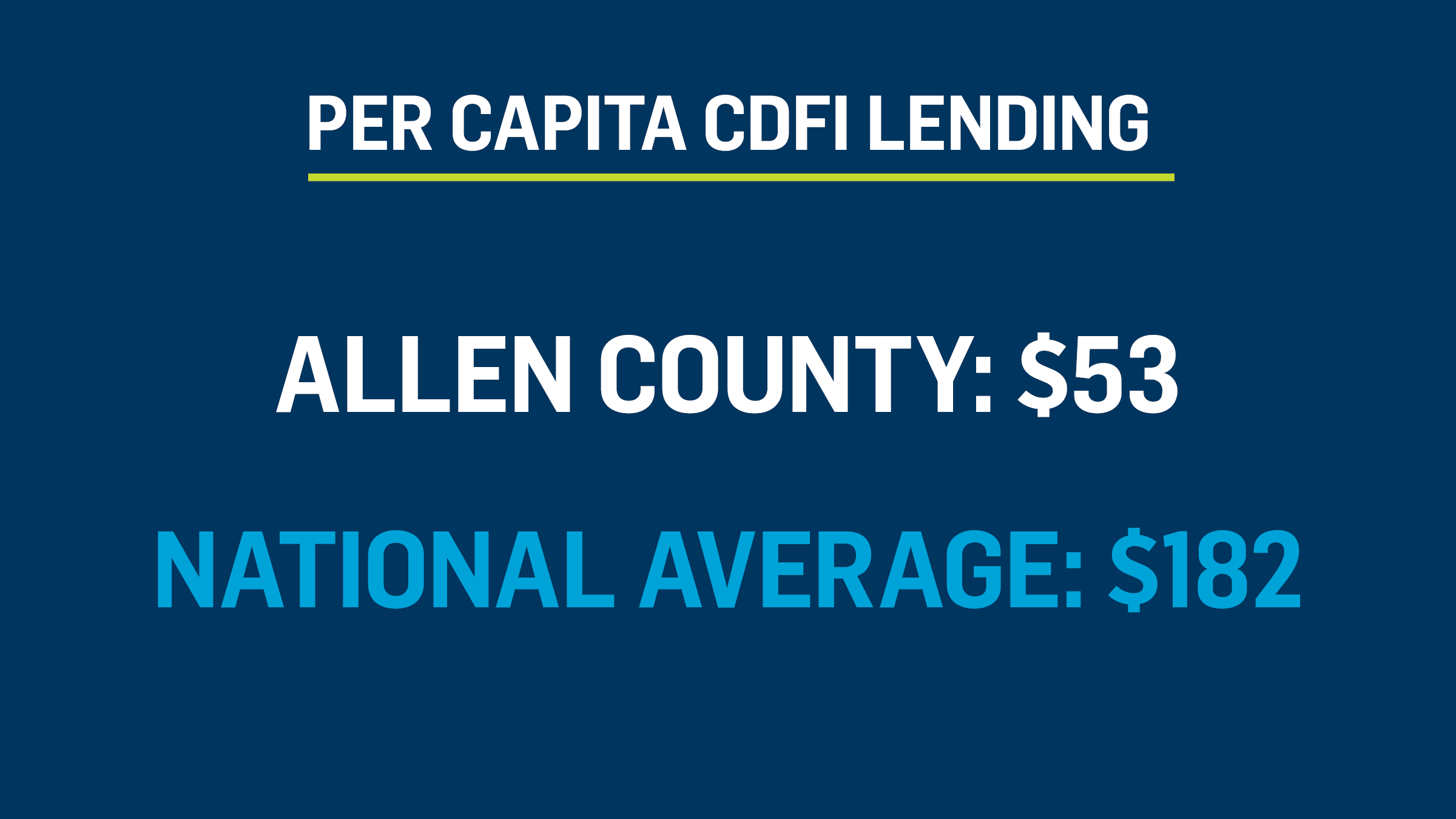

Fort Wayne has gaps in access to capital that need to be addressed, too, as evidenced by a Phase-1 study from CDFI Friendly America. The study showed local CDFI lending activity in recent years is just 30 percent of the national average, says Ellen Cutter, Chief Economic Development Officer for Greater Fort Wayne Inc.

![]() According to Greater Fort Wayne Inc., Allen County trails behind the national average in terms of per capita CDFI lending.

According to Greater Fort Wayne Inc., Allen County trails behind the national average in terms of per capita CDFI lending."It showed us that clearly some entrepreneurs and small business owners aren’t being served," she says.

Other than Brightpoint, Fort Financial Federal Credit Union is the only other CDFI currently in Northeast Indiana.

“Now the challenge is: How do (we translate) the information and feedback from the participants in those surveys and focus groups?” Little asks. “And how can we deploy more CDFI-type instruments into our community to provide these opportunities for folks who are not getting that opportunity right now?”

Little says in working with the team at Greater Fort Wayne Inc., they’ve met with CDFI institutions from around Indiana and Illinois. Right now, they’re in the “homework” phase in trying to determine how to bring additional CDFIs here and determining what that might look like, on a practical level.

John Urbahns, President and CEO of Greater Fort Wayne Inc., offers context on how this work fits into the larger picture of the

Allen County Together Plan. This blueprint spells out the pathway to invest in initiatives in Northeast Indiana that build an inclusive and nationally recognized economy. Under the pillar of inclusion, Urbahns says a priority is to close the disparity gap by providing financing to underserved individuals and small businesses via expanded CDFI capacity. To that end, it means deploying $10 million in funding by 2026 and $25 million in funding by the end of 2031.

![]() Urbahns

UrbahnsAt the same time, he says they don’t want to reinvent the wheel.

“Right now, we’re in conversations with CDFIs that have identified Fort Wayne and Allen County as part of their target market area, even though they may or may not have done work here in the past,” Urbahns says. “We're trying to increase those relationships to create opportunities to draw additional CDFI funding in without creating a new CDFI. If there's somebody out there who will serve our area, we should be leveraging that as a starting point.”

This story is made possible by underwriting support from Greater Fort Wayne Inc.